What Is Considered A Good Credit Score?

The question What is considered a good score is not as simple as giving out a number.

The question What is considered a good score is not as simple as giving out a number. This is because there’re tons of different credit scores out there, and to make matters worse, different lenders have different criteria for a good credit score!

I know, sounds complicated already, so allow me to provide a little bit of clarity to the question 😊

How the FICO credit score works

The FICO Score 8 is the most commonly used credit score model, by far, so we’re going to focus on this model in this article. The score ranges from 300 to 850, and the higher the score the better.

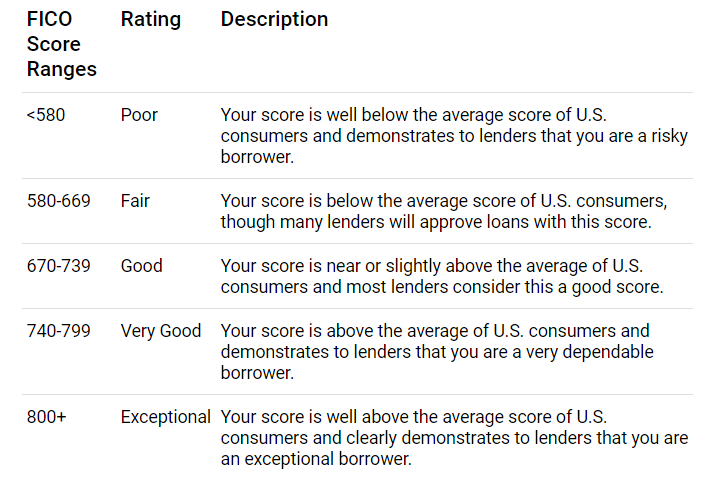

According to myFICO.com, here are the credit score ratings:

Source: myFico.com

Here’s the quick version of the FICO bands so you don’t have to squint at the chart:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very good: 740–799

- Exceptional: 800–850

As of 2026, the average FICO score in the U.S. sits around 717 — near record highs, and a good chunk above where it was a few years ago. So a “good” score generally starts in the 670–739 range, and anything 740+ is where you start unlocking the best interest rates lenders offer.

What determines the credit score?

How the credit score itself is determined is one of the best-kept secrets of the modern age! I still don’t know how they have managed to keep the formula such a secret. We do know the different categories that contribute to the overall credit score:

- Payment History: Are all your bills paid on time every month?

- Credit Utilization: How much do you owe your creditors relative to your total credit limit?

- Age of Credit: How long have you had your credit cards and loans open?

- Credit Inquiries: How many new accounts are you opening and have you been applying for new cards?

- Credit Mix: Are you able to responsibly juggle different types of accounts (credit cards, mortgage, auto loan)?

Let’s take a closer look at these aspects and how they affect your credit score.

1. Payment History (35%)

There isn’t a formula that goes with your payment history. Simply put, do you pay all your credit bills on time and every single month without fail? This category makes up the bulk of your credit score. A single missed payment can cause your credit score to tumble down! So make sure you always pay your credit card bills on time, every time!

2. Credit Utilization (30%)

This is the second biggest category when it comes to your credit score. The formula is pretty simple.

- Add up the balances on all your credit cards

- Add up the credit limits on all your cards

- Divide the total balance by the total credit limit

- Multiply by 100 to see your credit utilization ratio (as a percentage)

This number is very important as it tells lenders if you are spending your maximum credit limits. This doesn’t look good on your score, so Experts always suggest you spend no more than 30% of your limits. The lower, the better!

3. Age of Credit (15%)

This considers various aspects of your credit picture by looking at the age of your individual credit accounts. The older your credit cards, loans, etc, the better it looks on your score. This is because you would have proven that you are capable of maintaining your accounts over an extended period of time.

4. Credit Inquiries (10%)

Whenever you apply for a new credit card or loan, the lender performs what is known as a Hard Inquiry, and that dings your credit score a bit. The more the dings, the more it adds up! So only actually go through with a credit application if you absolutely have to.

5. Credit Mix (10%)

Lenders like to see credit holders being able to juggle different types of accounts on their credit reports. So having a mixture of credit cards, car loans, mortgages, etc, has a positive effect on your score.

What’s my credit score?

Many credit card companies offer free credit score checking to their customers, but not all.

I personally use Credit Karma to get a general idea of what my credit score is, so I recommend you sign up and take a look for yourself to see what your credit score looks like:

![]()

How can I increase my credit score?

A good Credit Score is built over time. There are no quick and easy tricks to game the system, but with perseverance, you can build a great credit score. I always mention to people that you can go from literally 0 to a great credit score.

The way to do that is to pay very close attention to your credit and make sure you kill it on the 5 categories listed above. It will take several years, but with discipline and dedication, any credit score can be improved.

For a quick win on the utilization side, see our guide on how to boost your credit score with one move. And if you’re eyeing a loan or mortgage soon, your score is only half the picture — lenders also weigh your debt-to-income ratio, so it’s worth checking yours before you apply.