Here's How To Buy A Home With Student Loan Debt

According to recent surveys, debt is the number one reason people, especially Millennials, aren't buying homes. But it's far from impossible.

According to recent surveys, debt is the number one reason people, especially Millenials, aren’t buying homes. The thing is though, as long as you have a manageable student loan balance, good credit, and a good income, you can still buy a home despite having student loans!

Today, more than 2 thirds of college graduates have some sort of student loan debt. Some are higher than others, but debt nonetheless. The good news is, lenders are still willing to take into account the student loan debt in determining eligibility to getting a mortgage.

Quick reality check before we dive in: the borrowing landscape has shifted a lot since I first wrote this. Federal student loan payments and interest resumed in late 2023 after the pandemic pause, so that monthly payment is back on your books — and mortgage rates that used to sit around 3% are now closer to ~6.5–7%. Both of those make the monthly math tighter, which is exactly why running real numbers (instead of guessing) matters more than ever. 🧮

So today, we’re going to look at some creative ways you can buy a home, despite having student loans.

1. Improve your credit score

This is the single most important thing lenders look for when qualifying you for a mortgage. A credit score is just like the test scores you took in school. The higher your score, the better you can handle your money (in theory). You can read more about credit scores here.

So the first thing you need to take a look at is your credit score. Most lenders require at least a 640 credit score, to qualify for a mortgage. If your score is at or above that score, you have good chances of qualifying for a mortgage. But this is just the beginning. There are a few more things to take into consideration that will help you qualify for your mortgage.

2. Get a good down payment

Here is where a lot of people get stuck and get scared away from getting a mortgage to buy a home. One thing to remember is that you don’t need to have 20% as a down payment. There are different loan programs, depending on your lender, that offer mortgages ranging from 0%, 3.5%, and 5%.

Chances are though, if you have a really high student loan balance, the lender might require a larger down payment. This not only demostrates that you’re serious, but it gets you to put more skin in the game (more money to lose, if you ever foreclose), and lowers your monthly mortgage payment. This is because you will have lowered the amount you’re borrowing by putting more money down.

So talk to your lender, and see what you can do regarding your down payment that will make you more favorable. And while you’re at it, drop your target price, down payment, and today’s rate into our mortgage calculator — it’ll show you exactly how a bigger down payment shrinks that monthly payment. Seeing the numbers side by side makes the decision a lot easier. 💪

3. Lower your income to debt ratio

It’s not as complicated as it sounds! Trust me :) Basically, your income to debt ratio takes into account your monthly gross income, and divides it by all your monthly payments.

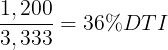

So for example, if you earn $40,000 a year, your gross monthly income is $3,333. If the total of all your monthly debt payments (student loan payments, credit card payments, personal loan payment, car payment) is $1,200 per month, then your Debt to Income Ratio is:

With a 36% DTI, you could qualify for a mortgage, but depending on how much the new debt would increase your DTI, you might not qualify. Lenders typically look for a DTI of less than 42%, but it’s always recommended to keep it below 29%! Don’t want to do the math by hand? Skip the formula and just run your own numbers through our debt-to-income calculator — punch in your income and monthly debts and it spits out your ratio instantly, so you know exactly where you stand before a lender ever pulls it up.

Instead, in this scenario, you can work towards lowering your monthly debt payments by selling off the car, paying off the credit card debt, or consolidating your student loans and have a lower monthly payment.

4. Increase your income

You’re probably thinking this is way easier said than done, but i’m here to tell you that it really isn’t that difficult.

There are multiple ways you can increase your income, and by doing so, increase your buying power and allowing you to afford to buy a home. A few ways you can increase your income might be:

- Doing side hustles that are consistent

- Investing in real estate

- Changing your job for a higher paying one

- Invest in earning passive income

- Apply for a mortgage Jointly with your spouse

These are just a few examples of ways you can increase your income that i’ve already written about! Before you roll your eyes, and move on to the next point, take the time to read on them and see if it’s something you can do. You stand to lose nothing when you try, but lose everything when you don’t try.

5. Apply for a mortgage pre-approval

Getting an actual pre-approval letter from a lender can help you fully understand what you can actually afford, and all the costs associated with buying a home.

Thing is, you could speculate and guess whether you can afford a home and whether a lender will approve you for a mortgage. But until you actually go through the process, you can’t always know for sure. So if you want to know if your student loans will allow you to buy a home, you will need to go through the approval process first.

So take the time to go to your favorite bank or credit union, and begin the application process. Getting your credit checked will ding your credit a few points, but that’s temporary, and it will give you peace of mind knowing what was missing and where exactly you can improve.

Here are some important points to remember when getting pre-approved for a mortgage:

- A pre-approval does not guarantee you a loan. It’s just a lender giving you a quick glance at your finances and giving you a thumbs up or down

- A pre-approval does affect your credit, as it counts as a hard credit pull. So do it sparingly

- The lender will ask for verification like bank statements, pay stubs, and tax returns. Be sure to have these, and more, ready for them

Once you have a pre-approval, then you can have a solid idea of how much house you can actually afford.

6. Get down payment assistance programs

Sometimes, it’s not the mortgage payment that deters many from homeownership. Sometimes, it’s the down payment that stops you. The good news is, there are quite a number of down payment assistance programs that can help you buy a home.

There are some federal loan programs like the FHA loan, that allows you to get a mortgage with as little as 3.5% down. There are also USDA loans you can use, depending on the area you live (such as rural areas), and even VA loans if you are in the military.

There are quite a number of options you can look into, so use the services of a mortgage broker (quick google search can find you some in your area). They are qualified to give you all the options and get a great mortgage that’s right for you.

Nothing quite like moving day!

So, should you buy a home despite having student loans?

That there, is completely up to you. There is no one answer fits all, as everyone’s situation is different.

The thing is, you need to be okay with carrying two large debts and keeping up with the payments for both. To the lender, all they are primarily concerned about is:

- How much money do you earn?

- Is your job secure?

- Can you handle all the monthly payments, with money left over?

- Do you have any cash set aside, just in case?

So not only should you meet these items above, you need to review your own priorities and see how homeownership stacks up. So can you buy a home despite having student loans? Absolutely!

So remember, increase your income, lower your debts, keep up with your payments, clean up your credit score, and you’ll build all the strengths needed to manage a mortgage.

And before you start house hunting, do yourself a favor and run the two numbers that matter most: your debt-to-income ratio and a realistic monthly mortgage payment at today’s rates. If you want to keep an eye on the whole picture — debt payoff, savings, net worth — our free money dashboard ties it all together so you can watch yourself get mortgage-ready. Good luck! :)